The world of investing often feels like a secret club with its own language and complex rules. You hear whispers of stocks, bonds, and portfolios, and it's easy to feel intimidated, even overwhelmed. But here's the truth: investing isn't just for the wealthy or the financially savvy. It's a powerful tool for anyone looking to build a secure future and grow their money. This article, "Investment Basics for Beginners: A Step-by-Step Guide," will demystify the process, offering clear, actionable steps to help you start your investment journey with confidence.

Why Invest? It's More Than Just Saving

You work hard for your money, and saving it is a smart first step. But simply stashing cash under a mattress or even in a low-interest savings account won't get you far in the long run. Why? Inflation. That silent killer erodes your money's purchasing power over time. A dollar today won't buy as much tomorrow.

Investing, on the other hand, puts your money to work. It gives your savings the chance to outpace inflation and generate additional returns, thanks to the magic of compounding. Compounding means your earnings start earning their own returns, creating an exponential growth effect. Think of it like a snowball rolling downhill – it gets bigger and faster with every turn.

Consider this: historically, the S&P 500, a common benchmark for the U.S. stock market, has delivered an average annual return of around 10-12% over long periods. Your savings account probably offers a fraction of that. If you're serious about financial independence and building real wealth, investing isn't optional; it's essential.

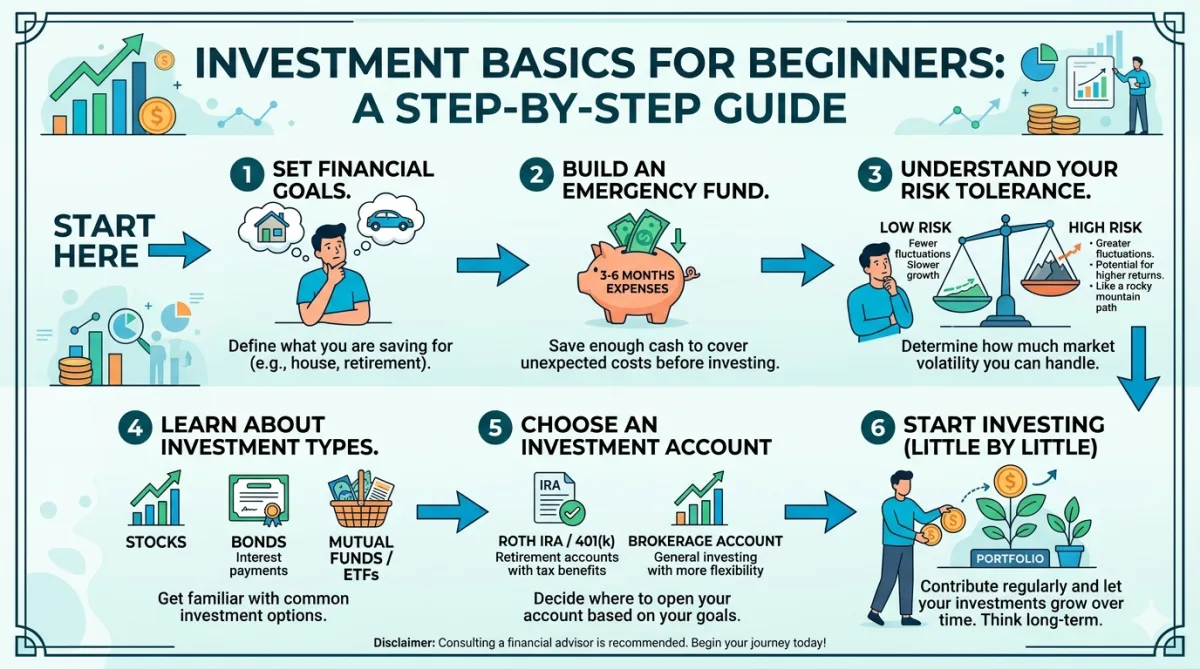

Your First Steps: Building a Strong Foundation for Investment

Before you even think about buying your first stock, you need to lay some groundwork. Skipping these crucial steps is like trying to build a house without a foundation – it's destined to crumble.

- Build an Emergency Fund: This is your financial safety net. Aim for 3-6 months' worth of living expenses saved in an easily accessible, high-yield savings account. Life throws curveballs, and you don't want to sell investments at a loss because of an unexpected car repair or medical bill.

- Pay Down High-Interest Debt: Credit card debt, personal loans, or any debt with sky-high interest rates are financial anchors. The interest you pay on these debts often far outweighs any returns you could make from investing. Prioritize paying them off; it’s a guaranteed return on your money.

- Define Your Financial Goals: What are you investing for? A down payment on a house? Retirement? Your child's education? Each goal has a different timeline and risk tolerance. Clearly defining them helps you choose the right investment strategies.

Understanding Your Risk Tolerance

This is a critical, often overlooked, aspect of investment basics. Your risk tolerance is your comfort level with potential losses in exchange for potential gains. Are you someone who'd panic if your portfolio dropped 20% in a month? Or can you stomach volatility, knowing that markets tend to recover over time?

Your age, income stability, and time horizon for your goals all play a role. A 25-year-old saving for retirement in 40 years can generally afford to take more risks than a 55-year-old saving for retirement in 10 years. Be honest with yourself about how much risk you can truly handle without losing sleep. It's better to start conservatively and adjust as you gain experience and confidence.

Diving into Investment Basics: What Are Your Options?

Once your foundation is solid, it's time to explore the different avenues for growing your money. Here are some common investment vehicles you'll encounter:

- Stocks: When you buy a stock, you're purchasing a tiny piece of ownership in a company. If the company performs well, its value typically rises, and so does your stock price. You might also receive dividends, a portion of the company's profits. Stocks offer the highest potential returns but also carry higher risk and volatility.

- Bonds: Think of a bond as a loan you give to a government or a corporation. In return, they promise to pay you back your principal amount by a certain date and pay you regular interest payments along the way. Bonds are generally considered less risky than stocks, offering more stability, but their returns are typically lower.

- Mutual Funds & Exchange-Traded Funds (ETFs): These are fantastic for beginners. Instead of buying individual stocks, you buy a share of a fund that holds a diversified basket of many different stocks, bonds, or other assets.

- Mutual Funds are professionally managed, and you buy or sell shares at the end of the trading day based on their Net Asset Value (NAV).

- ETFs trade like individual stocks on exchanges throughout the day. They often track specific indexes, like the S&P 500, offering broad market exposure at a low cost.

Both funds offer instant diversification, meaning you're not putting all your eggs in one basket. If one company in the fund performs poorly, it won't derail your entire investment.

- Real Estate: This can mean buying a rental property, investing in a Real Estate Investment Trust (REIT), or even crowdfunding platforms. Real estate can provide income through rent and appreciation in value, but it's often less liquid and requires a larger upfront capital commitment than other options.

Crafting Your Portfolio: Diversification and Long-Term Vision

Building a "portfolio" simply means creating a collection of different investments. The key to a resilient portfolio, especially for beginners, is diversification. Don't just pick one stock and hope for the best. Spreading your investments across different asset classes (stocks, bonds), industries, and geographies reduces risk. If one area struggles, others might thrive, balancing out your overall returns.

Your asset allocation – the mix of stocks, bonds, and other assets – should align with your risk tolerance and time horizon. A common rule of thumb often suggested is the "110 minus your age" rule for determining your stock allocation. So, if you're 30, you might aim for 80% stocks and 20% bonds. As you get older and closer to your goals, you'll generally shift towards a more conservative allocation with more bonds.

Another powerful strategy is dollar-cost averaging. This means investing a fixed amount of money at regular intervals (e.g., $100 every month), regardless of market fluctuations. When prices are high, your fixed amount buys fewer shares; when prices are low, it buys more. Over time, this strategy averages out your purchase price and reduces the risk of trying to "time the market," which is nearly impossible for even seasoned pros.

What This Means For You: Taking Action and Staying the Course

It's time to translate knowledge into action. Here's what you need to do:

- Start Small, Start Now: Don't wait until you have thousands of dollars. Many brokerages allow you to start with just a few dollars, especially with ETFs. The power of compounding means that time is your greatest ally. The sooner you start, the more your money can grow.

- Automate Your Investments: Set up automatic transfers from your checking account to your investment account each month. This removes the temptation to spend the money and ensures consistent contributions, leveraging dollar-cost averaging without you even thinking about it.

- Educate Yourself Continuously: The financial world evolves. Keep reading, listening to reputable podcasts, and learning about personal finance. Understanding what you own and why you own it is crucial.

- Don't Panic Sell: Markets will go down. It's a guarantee. When downturns happen, resist the urge to sell everything in a panic. Historically, markets recover. Staying invested through volatility is often the best strategy for long-term growth.

Embarking on your investment journey might seem daunting at first, but remember, every experienced investor started exactly where you are now. By understanding the investment basics for beginners, building a solid financial foundation, diversifying your portfolio, and committing to a long-term vision, you're not just saving money; you're actively shaping your financial future. Take that first step, stay disciplined, and watch your wealth grow.